Managing your money doesn’t have to be complicated. One of the simplest budgeting methods that has stood the test of time is the 50/30/20 rule. But does it really work in today’s financial climate? Let’s break it down.

What is the 50/30/20 Rule?

Popularized by U.S. Senator Elizabeth Warren in her book “All Your Worth: The Ultimate Lifetime Money Plan”, the 50/30/20 rule offers a straightforward way to manage your monthly income. Here’s how it works:

-

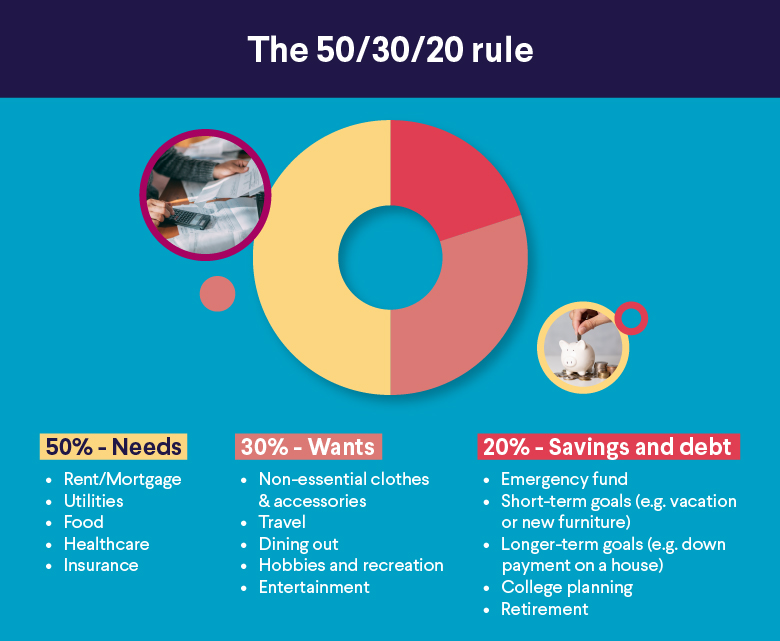

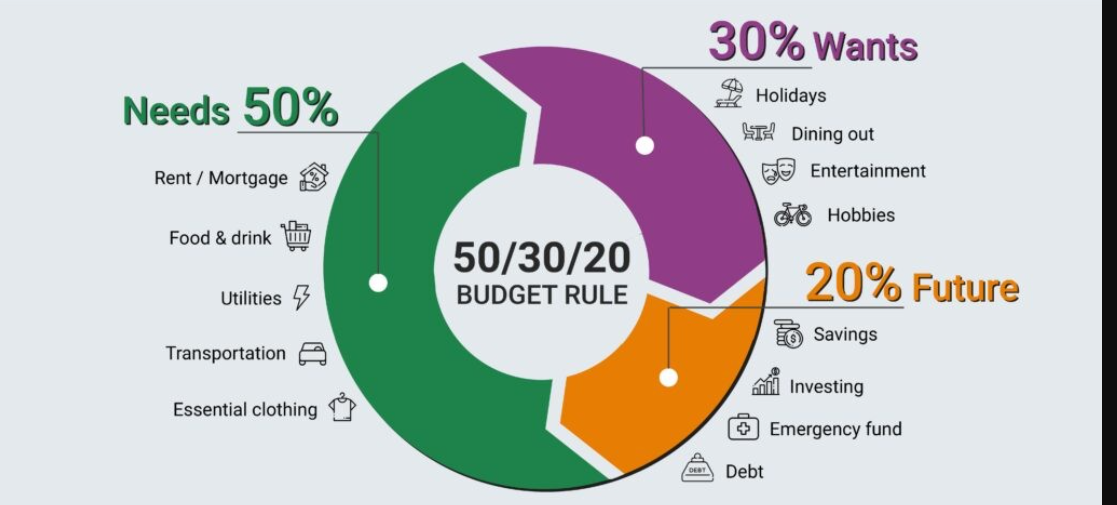

50% of your income goes to needs – These are essentials like rent, groceries, utilities, health insurance, and minimum debt payments.

-

30% goes to wants – This includes dining out, subscriptions, entertainment, shopping, travel, and other lifestyle choices.

-

20% goes to savings and debt repayment – This is for building your emergency fund, retirement savings, investments, and paying off debts beyond the minimum.

Why It Works

-

Simplicity

The rule is easy to remember and implement, especially for beginners. It doesn’t require complicated spreadsheets or advanced financial knowledge. -

Balanced Lifestyle

It acknowledges that life is not just about paying bills or saving. By allocating a portion for “wants,” it helps you enjoy your earnings while still staying on track financially. -

Focuses on Savings

Setting aside 20% for savings and debt reduction ensures you’re making progress toward long-term financial goals.

When It Doesn’t Work

Despite its strengths, the 50/30/20 rule may not be ideal for everyone, especially in these situations:

-

High Cost of Living

If you live in an expensive city or country, essentials like rent and transportation might take up more than 50% of your income, leaving little for wants or savings. -

Low or Irregular Income

For those earning minimum wage or freelancing without a stable paycheck, sticking to these exact percentages may not be feasible. -

High Debt Levels

If you’re deep in debt, allocating only 20% to savings and debt repayment might slow your financial recovery. -

Ambitious Financial Goals

If you aim to retire early, buy a home quickly, or invest aggressively, you might want to boost your savings rate well beyond 20%.

Making the Rule Work for You

The 50/30/20 rule should be seen as a guideline, not a strict formula. You can adapt it to fit your situation:

-

60/20/20 or 70/20/10: If your needs take up more of your budget, tweak the percentages accordingly.

-

40/20/40: If you’re focused on wealth building or debt freedom, increase your savings allocation.

-

Track, Then Adjust: Start by tracking your actual spending for a month. Use those insights to adjust the rule to match your reality.

Final Thoughts

The 50/30/20 rule is a great starting point for budgeting, especially if you’re looking to build financial discipline without overwhelm. However, it’s not a one-size-fits-all solution. Like any good financial strategy, it works best when it’s personalized.

Use it as a foundation—then adjust, refine, and grow from there. What matters most is that your money is moving in a direction that aligns with your goals and values.