For years, Safaricom has been seen as one of Kenya’s most reliable blue-chip stocks—a darling of retail investors and institutional portfolios alike. But a closer look at its performance between 2016 and 2025 tells a more sobering story: for many investors, the returns have been underwhelming, especially after factoring in inflation.

A Decade of Modest Gains

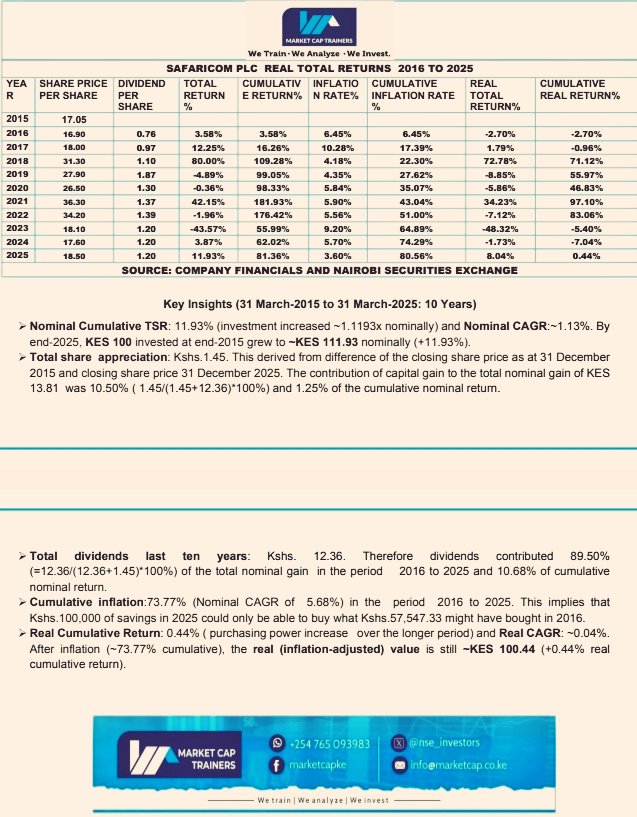

An investment of KES 100 in Safaricom shares in 2015 would have grown to just KES 112 by 2025. That’s a total return of roughly 11.9% over ten years—a figure that barely keeps pace with time, let alone risk.

When inflation is taken into account, the picture worsens. Over the same period, the Kenyan shilling lost approximately 73.77% of its purchasing power. In real terms, that leaves investors with a negligible return of about 0.44%, meaning their wealth has essentially stagnated over an entire decade.

Dividends Did the Heavy Lifting

The bulk of investor returns did not come from share price growth, but from dividends. Over the ten-year period, Safaricom paid out about KES 12.36 per share in dividends—accounting for nearly 90% of total returns.

In contrast, capital appreciation contributed very little. The share price moved from KES 17.05 in 2015 to around KES 18.50 in 2025, translating to minimal growth. For a company often perceived as a growth stock, this performance paints a different picture: Safaricom has largely behaved like an income stock.

The Shock of 2023

The year 2023 stands out as a particularly painful period for investors. The stock plunged by over 43%, wiping out years of accumulated gains and leaving many who bought near peak valuations deep in the red. For some, the recovery has been slow or nonexistent.

A Shift in the Narrative?

Despite the disappointing past decade, there are emerging factors that could reshape Safaricom’s future.

First is its expansion into Ethiopia. Through Safaricom Ethiopia, the company has entered a market of over 120 million people. While the venture has so far been loss-making, recent signs suggest it may be gaining traction. If the Ethiopian operation turns profitable, it could significantly alter Safaricom’s growth trajectory.

Second is the influence of Vodacom, now the majority shareholder. Known for its assertive dividend policies, Vodacom could push for higher and more consistent payouts, potentially making Safaricom even more attractive to income-focused investors.

The Bottom Line

Over the last decade, Safaricom has not delivered the kind of wealth creation many investors expected. Those who invested for steady income through dividends fared reasonably well. However, investors banking on strong capital gains were largely disappointed.

Looking ahead, the company’s story may be entering a new chapter. Ethiopia represents a high-risk, high-reward opportunity, while Vodacom’s influence could strengthen its dividend appeal.

The lesson is clear: past performance does not guarantee future results. Safaricom’s last ten years serve as a cautionary tale—but the next ten could yet become a story of recovery and growth.