Every parent wants the best for their children. Hence, we tend to be emotional when it comes to choices on their learning.

Education insurance policies use these emotions to profit from us and in the process many end up losing big time.

Many Kenyans may consider buying education insurance policies as one of their worst investment decisions.

These policies are often complex and difficult for the average person to understand and are sold by experienced salespeople.

At first glance, education insurance policies may seem like a good investment for your children’s education, but upon closer examination and consideration of other alternatives, they may not be worth the cost.

It is important to note that insurance is a product for wealth protection, not wealth creation. Education insurance policies, however, mix insurance and savings for your children’s education into one product. This can be misleading and lead to poor investment decisions.

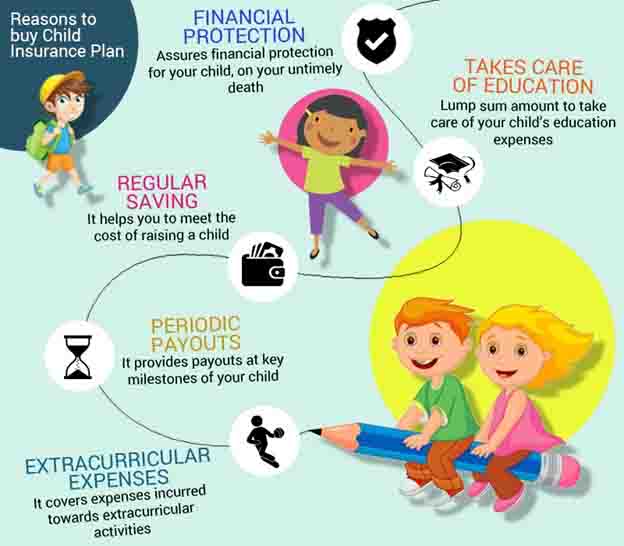

Definition of education insurance policy

An education insurance policy is a life insurance product that provides a payout for your child’s education in the event of the death or disability of a parent.

- Education policies can help you save consistently every month for important things like a child’s education. This can be a lifesaver given the high cost of fees, especially at the university level. It also helps to have a reminder every month to send your savings even if you are not doing it specifically for your children’s school fees.

- You can also get tax relief. This reduces the amount of tax you pay monthly. In Kenya, every resident individual is entitled to an insurance relief of 15% of the value of premiums paid, subject to a maximum of KES 60,000 p.a. The education policy must also have a maturity period of at least 10 years.

The high cost of education and fear for the future of your children may make these policies appealing, but there are other options to consider.

It’s better to consider taking independent insurance coverage against death, disability or chronic illness, and investing in other asset classes like money market funds, stocks, real estate, and treasury bonds for wealth creation.

These options may provide better returns and be more cost-effective in the long run.

https://twitter.com/kahome_steve/status/1616676570525011968?s=20&t=8peSVDjjYy-ujGljZg-YhQ

Why Education Insurance Polices are Poor Products

But when you look at it critically, the policies aren’t what they are said to be. In fact, they are worse.

There are several reasons why education insurance policies are considered poor products:

- They mix insurance, savings, and investments in one basket: This can be misleading and lead to poor investment decisions as wealth creation and protection are two different things that should not be mixed.

- The policies are complex and difficult to understand: The average person may find it challenging to fully understand the terms and conditions of education insurance policies, making it difficult to make informed investment decisions.

- The policies may not provide enough return on investment: The return on investment for education insurance policies may not be enough to justify the cost, especially when compared to other investment options.

- The policies are often sold by experienced salespeople: Insurance agents may use high-pressure sales tactics and instill fear to convince people to buy education insurance policies, leading to poor investment decisions.

- Alternative investment options may be more cost-effective: Instead of investing in education insurance policies, it may be more cost-effective to take independent insurance coverage for death, disability or chronic illness, and invest in other asset classes like money market funds, stocks, real estate, and treasury bonds for wealth creation.

Conclusion

Education insurance policies are considered as poor products for several reasons, as we have mentioned above. The problem is that they are normally sold as the only way parents can successfully manage paying for school fees without any stress, whether alive or dead.

Therefore, it is not advisable to buy education policies. It’s important to consult a financial advisor or do your own research to find the best investment options for your future goals.